Recursive Self-Improvement isa Portfolio Optimization Problem

York Westenhaver·Massey Branscomb·Aidan Grant

AlphaFund

Abstract

Recursive self-improvement is usually framed as software rewriting itself. We propose a narrower, measurable formulation: a corporation recursively improves when realized economic gains finance the next cycle of better prediction and deployment. Quantitative trading instantiates this loop with unusual precision, since decisions, costs, outcomes, and reinvestment are all digitized. We introduce the Economic World Model (EWM), a forecasting and control object scored on future realized outcomes, and summarize the firm’s standing as t-RSI, a standardized gap between alpha-creation and alpha-decay rates. We present evidence of the first general economic scaling law beyond language data; further evidence from live trading and held-out backtests support the framework. We position today’s firm as the present-moment derivative of a trajectory toward an Autonomous Self-improving Corporation (ASIC), in which capital allocation is itself executed by the firm’s software. Thus, recursive self-improvement can be reframed as an auditable capital-allocation process.

Introduction

The literature on recursive self-improvement spans decades, from Yudkowsky’s seed AI framing [1], through Schmidhuber’s Gödel Machines [2], to formal and empirical treatments of recursive self-improvement and intelligence explosion dynamics [3, 4, 5], to more skeptical analyses emphasizing diminishing returns and bottlenecks [6]. These formalisms differ in mechanism, but they share a simplifying assumption: the economic costs of the improvement step do not threaten the system’s existence. In reality, every FLOP and bit of data costs money [7, 8, 9]; self-improvement is an economic problem.

In the same way that biological organisms need resources and a suitable environment to survive and evolve [10, 11], the more complex system of the global economy needs capital to do the same [12]. A system that spends more on self-improvement than it earns from the resulting improvement slowly runs out of resources and dies. We thus define intelligence operationally: the capacity to acquire, preserve, and compound command over resources through accurate prediction. Because the environment is non-stationary and uncertain, the question shifts from whether RSI will occur to whether a system can generate sufficient capital to fund each attempt at self-improvement. This reframing casts recursive self-improvement (RSI) as a stochastic control problem under a survival constraint, with progress scored by the standardized signal-to-noise ratio of expected improvement against its posterior dispersion—a quantity we call t-RSI. For AlphaFund at the current operating point, the data-derived three-month t-RSI is 9.61 standardized units. It should be made clear that RSI is impossible to guarantee. The position and momentum of a particle can’t be known; a gamma-ray burst from across the universe could wipe all life out. We are proposing a concrete and measurable framework that allows researchers to talk about this hypothetical phenomenon in a grounded and empirical manner.

We develop this claim in five steps:

The Self-Improving Corporation. We formalize the corporation as stochastic optimal control under a balance-sheet survival constraint, specifying the state, transition law, objective, and capital-allocation program that convert predictions into a reinvestment process.

The Economic World Model. We decompose this theoretical problem into a practical prediction architecture and show that, under the channel coupling we make explicit, the decomposed system recovers the same first-order conditions as a joint-monolith optimum at the operating point.

The Portfolio Optimizer. We define the corporation’s controller as a model-predictive convex program over the EWM’s per-channel return forecasts, making heterogeneous interventions — a researcher hire, a data feed, a GPU, a position in AAPL — directly comparable.

The RSI Portfolio. We instantiate that controller channel by channel — investments, sensors, actuators, parameters, R&D — and present the empirical scaling and response laws that pin down each row of the marginal-return vector.

Trajectory. We study the long-run dynamics of the controller under those scaling laws—accounting for complementarity, filtration widening, and external capital—and argue that, if the preliminary laws hold under continued validation and marginal deployment keeps clearing after capacity, competition, financing, and market-impact costs, this process could plausibly capture a substantial share of financial-industry profits and serve as a bridge from quantitative trading toward broader priced economic action.

The Self-Improving Corporation

Corporations are intelligent self-improving systems. They can replace their own personnel, hardware, software, board, and even their business model and still retain their core identity—the legal name for this property is perpetual succession. Like the Ship of Theseus, what matters is not that any given component persists, but that the process that turns capital into improved capability and improved capability back into capital persists through continual reconfiguration. Most corporations do not, in fact, recursively improve; the question this paper asks is what conditions distinguish those that do. All for-profit corporations share the same objective: maximize shareholder value while remaining solvent [13, 14]. In service of that objective they observe their environment and internal state, allocate capital across operational capabilities, receive feedback in the form of earnings, and reinvest those earnings to augment future capability. We mean capital in the most generic sense: resources necessary to survive and improve. Dollars are generally fungible for those, and thus represent a satisfactory scalar approximation.

We model this sequential optimization process—the Corporate Loop—as constrained stochastic optimal control over the firm’s production cycle [15, 16, 17]. Quantitative trading is the cleanest case: its feedback loop is fast, direct, and dollar-denominated, and its production, sales, capital allocation, and reinvestment functions can all be specified precisely and measured at high frequency. The four subsections below set the four pieces the rest of the paper composes: the firm’s objective, the asset bundle the objective is computed over, the action vector that moves that bundle, and the coupled dynamics under which the bundle and the world evolve together.

Firm Objective and Accounting Identity

For-profit corporations exist to maximize shareholder value subject to remaining solvent [13, 14], and shareholder value is, by construction, shareholders’ equity—the residual claim on assets after liabilities are netted. The firm’s per-period reward is the realized log-return on that equity [18], the survival constraint is Kτ>0, and the cumulative objective Jt is the expected sum of those per-period rewards over a finite planning horizon. All later channels are priced against this Jt.

Definition 1Shareholders' equity

Shareholders’ equity at decision time t is the firm’s net worth: total assets minus total liabilities, marked to current dollars.

Kt=Assetst−Liabilitiest

Definition 2Per-period reward

The per-period reward at cycle τ is the realized log-return on shareholders’ equity from τ to τ+1. Log-returns track the Kelly time-average growth rate of a single surviving firm [18, 19]. The strict positivity Kτ>0 is the firm’s survival constraint: a trajectory in which equity hits zero is bankruptcy.

Rτ=log(KtKt+1)

Example

Suppose the firm has $100 of equity at time τ and $110 at time τ+1. Then Rτ=log(110/100)≈0.095—the firm earned $10 on $100 of equity over the cycle.

Definition 3Cumulative objective

The cumulative objective at decision time t is the expected sum of per-period rewards over a finite planning horizon T, taken under the firm’s policy G and its learned world model Wt, conditioned on the information available at t. It is a Discounted Cash Flow calculation over the foreseeable time horizon; how T is calibrated is discussed in the next section.

Jt=EG,Wt[τ=t∑T+t−1RτFt]

Example

Suppose at decision time t the firm has $100 in equity value of its assets and its world model forecasts those to rise to $110 over a one-cycle horizon (T=1). Then J1=E[log(Kt+1/Kt)]=log(110/100)≈0.095, or—in the dollar-equivalent form used throughout the rest of the paper—an expected $10 gain on $100 of equity.

The Corporation as a Bundle of Assets

To execute its optimization the corporation maintains an inventory of operational components—the channels through which it spends capital, generates the cash flows that keep it solvent, and earns capital back. Five channels suffice: what the firm holds (I, portfolio), what it can see (S, sensors), what it can do (U, actuators), how it learns (Z, R&D), and what it knows (Θ, parameters). We adopt a lossy five-channel partition that suffices for the quant-trading instance and that we will argue extends to the general case. The framework only requires that each row can be priced in dollars and that channel-specific scaling laws are estimable from the firm’s history.

The action vector at partitions the cycle-t change in the corporation into the same five channels as the state; each entry atk is the dollar change in channel k during the cycle (Action vector). The symbol-by-symbol definitions of the five channels are given via the projections in Corporation tuple and Action vector.

Definition 4Corporation tuple

The corporation is an abstract object. The state projection πstate partitions that object into the five channels that reflect the stock of capabilities that a corporation has at each decision time t:

Πstate(Ξt)=ItStUtΘtZt

Corporation tuple Ξt components.

Symbol

Channel

What it is

It

Portfolio

The vector of current resources that the corporation can sell to produce cash. In a trading firm this is tradable asset positions across equities, fixed income, commodities, currencies, derivatives, and other instruments.

St

Sensors

Data and feeds that bring information about both the firm and the outside world to light. For a trading firm this includes market data feeds, internal execution telemetry, satellite feeds, and social media data.

Ut

Actuators

Instruments the firm uses to modify the world. For a trading firm this includes the different assets it can trade, APIs it can call, types of financing it can access, AUM, margin, and equity.

Zt

R&D

How the firm processes new information and improves the other channels. For a quantitative trading firm, this determines the values for its parameters based on training data: the research process, experiment harnesses, and model selection infrastructure.

Θt

Parameters

Accumulated learned structure that represents the firm’s current beliefs about available transformations. For a quantitative trading firm, these are the parameters of the firm’s forecasting, execution, control, and value models.

Definition 5Action vector

The action vectorat partitions the cycle-t change in the corporation into the same five channels as the state. Each entry atk is the dollar change in channel k during the cycle:

Πact(at)=atIatSatUatΘatZ

Capital-allocation vector at components.

Symbol

Channel

What it is

atI

Investments

Net dollars rebalanced into (or out of) the trading book this cycle. The cleared trade, marked to current cash.

atS

Sensors

Cash spent acquiring data this cycle: new feeds, deeper archives, finer-grained subscriptions.

atU

Actuators

Cash spent extending the firm’s execution surface: new venues, routes, APIs, financing capacity.

atZ

R&D

Cash spent on researcher labor and capital-substitutable research: agents, GPU-hours, search infrastructure, sealed-holdout tooling.

atΘ

Parameters

Cash spent on training compute that produces the next set of model weights.

Coupled Dynamics

The environment Et is the part of the world outside the corporation that matters for the next cycle: prices, order flow, liquidity, counterparties, macro state, regulation, and the news process. Coupled dynamics states how the corporation and that environment move together after the firm acts.

Definition 6True corporate transition

The true joint transition lawW governs how the firm’s state Ξt and the environment Et co-evolve under an action at. It is a property of the world, not a model the firm has access to; the firm must approximate W with a learned Wt (Economic World Model).

(Ξt+1,Et+1)=W(⋅∣Ξt,Et,at)

Example

The world turns. The clock ticks, prices update. The corporation’s sensors measure these changes.

The small-firm approximation is the regime in which the environment’s next-cycle state Et+1 depends only weakly on the firm’s action at:

∂at∂Et+1≈0.

Suppose George Soros, in September 1992, shorts £10B against the Bank of England’s peg. The trade itself drains the Bank’s reserves; the next trade drains them faster; the pound’s market price collapses, and Soros makes a fortune [20]. When you are large enough to affect the market, the small-firm approximation no longer applies.

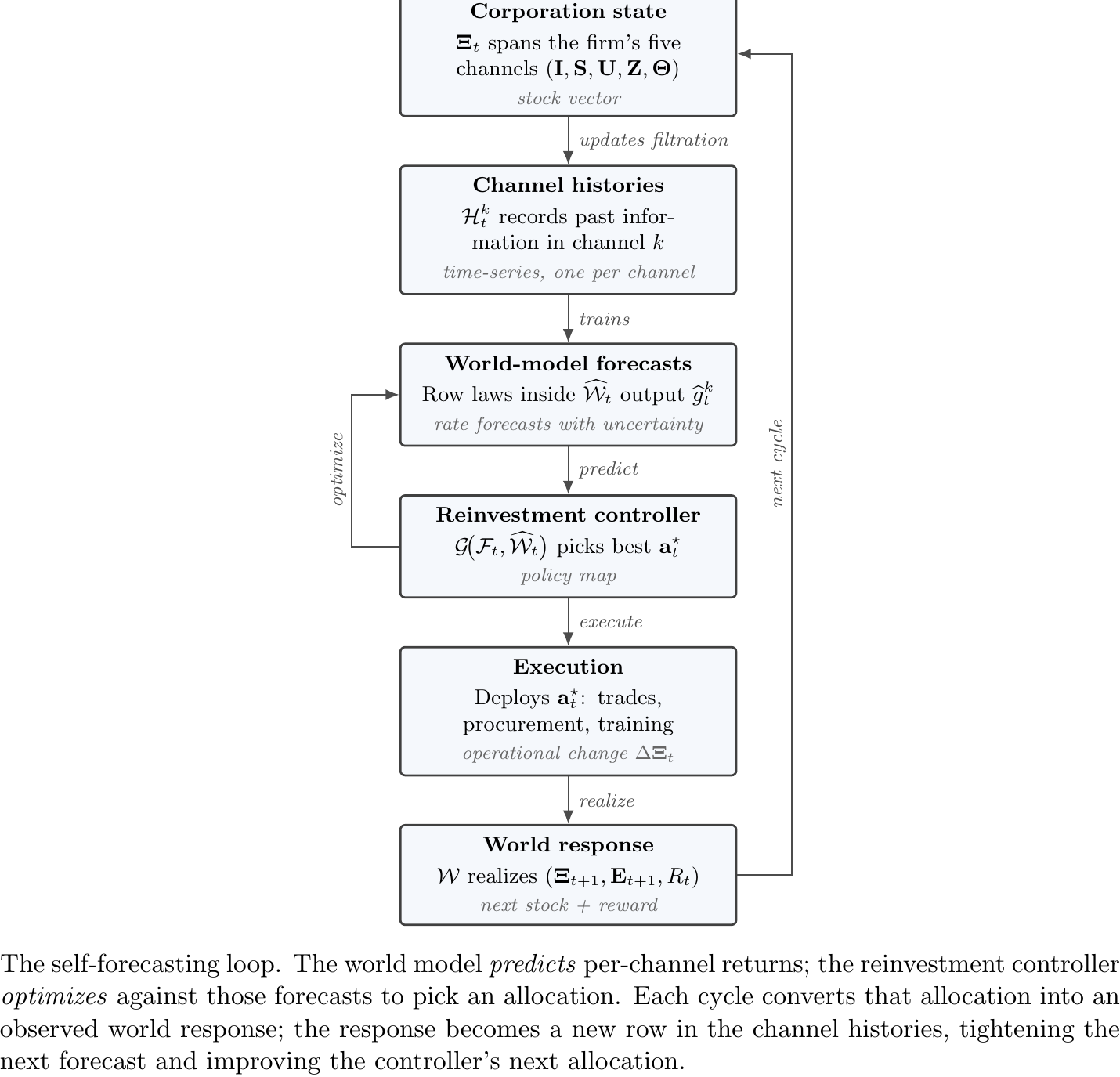

The Self-Forecasting Loop

Figure 1. The self-forecasting loop. The world model predicts

Every operating cycle appends one row of observations to each channel history Htk. The sensor channel can additionally widen by adding new data: Wayback Machine snapshots, exchange filings, alternative-data archives. Each turn provides the next iteration of training data.

Once enough rows accumulate, accurate predictions can be made on a channel-by-channel basis, allowing the firm to predict its own self-improvement dynamics. In theory, a unified world model would be trainable with enough data such that the firm could jointly predict its own state, improvements to it, and the state of the external economy all at the same time.

Concretely: at decision time t the controller queries the world model for gt off the trained row laws (predict), solves the convex inner program of Portfolio Optimization to pick the best action (optimize), executes the chosen at⋆, and the realized (Ξt+1,Et+1,Rt) becomes the new training row that tightens the next cycle’s forecasts.

Each improvement attempt teaches the firm something about itself. The action it took, the internal change it produced, and the reward that followed become a new row in the channel histories. As those rows accumulate, the firm gets sharper predictions about which future improvements will work and tighter confidence intervals around the value of its own next actions. The loop is the thesis of the paper compressed into one diagram; everything that follows is one of these arrows worked out in detail.

The Economic World Model

The previous section gave the firm a state, a coupled dynamics W, and a constrained optimization problem over a planning horizon. What it did not give the firm is a way to evaluate candidate allocations: given that the controller takes action at now, what does the next (Ξt+1,Et+1,Rt) look like? The true law W answers that question in principle, but W is a property of the world, not something the firm has access to. The firm must build its own learned approximation. We call that approximation the Economic World Model (EWM)—a world model in the control and planning sense, a learned object used to roll forward possible futures under candidate actions [21, 22, 23, 24, 25, 16, 17]. The qualifier economic marks a structural feature, not a stylistic one. The EWM is trained on a prediction-error loss (Empirical EWM estimator), but every input that lowers that loss—data, compute, parameters, refits, R&D campaigns—is itself priced in dollars on the firm’s books, and every reduction in predictive loss flows back into the firm’s expected return rate. The subsections below define the EWM, contrast it with a language model trained on a static snapshot, and lay down the channel histories that make per-channel scoring tractable.

EWM Definition

The EWM is the conditional next-cycle law the firm uses to forecast the joint (Ξt+1,Et+1,Rt) given its current information set Ft and a candidate action at. It is the only model of the future the firm has access to, so improving it is itself an allocation with first-order effect on Jt.

Definition 7Economic World Model

The Economic World Model (EWM) is the firm’s learned, filtration-respecting approximation to W. Given the information set Ft and a candidate action at, Wt returns a joint distribution over the next firm state, the next environment, and the cycle reward. Improving Wt is itself an allocation:

(Ξt+1,Et+1,Rτ)=Wt(⋅∣Ft,at)

Example

Suppose the corporation has a large transformer neural network that consumes supply-chain telemetry and geopolitical news; the firm uses that network to forecast how an Iran conflict will change oil prices, how those oil prices will change the value of the firm’s futures contracts, and what effect that change will have on shareholders’ equity.

Firm and Channel Histories

Because the firm sees the world only through its sensors, both Et and its own state Ξt enter the EWM as posteriors over noisy observations rather than as latent ground truth. The firm history Ht is the chronological log of every observation through cycle t—the canonical sufficient statistic in the partially-observed Markov decision process tradition [26, 27, 28, 29]. The channel histories Htk slice it channel by channel into (oτk,aτk,Rτ+1) rows. These per-channel slices are the tables the firm uses to fit the row laws of the marginal-return vector.

Definition 8Firm history

The firm history at time t is the chronological observation–action–reward log the firm has recorded through cycle t. The observation vector oτ is the sensor output generated by the latent corporation–environment state; the action aτ is what the firm did next; and Rτ=log(Kτ+1/Kτ) is the cycle-τ reward realized after that action.

Ht=o0o1⋮ot−1ota0a1⋮at−1–R1R2⋮Rt–

Definition 9Channel history

The channel history for channel k at time t is the channel-k slice of Ht, recording for each cycle in the firm’s lookback window the channel observation oτk, the channel action aτk, and the next realized log-equity reward.

Suppose the firm keeps a sensor-channel history of every dataset it has owned. Each row records the data inventory available before the cycle, the dataset or feed acquired in that cycle, how that data set improved backtests on different candidate models, and how much live trading was improved, as well as counterfactual simulations of what would have happened had the firm not acquired that data set.

Definition 10Firm filtration

The firm filtration at time t is the σ-algebra generated by the firm history. A random variable is Ft-measurable iff its value is determined by Ht. The family {Fs}s≥0 is what enforces the no-peeking discipline of the EWM: a forecast at time t may condition on Ft and on nothing resolved later.

Ft=σ(Ht)

LLMs are not economic world models

The filtration requirement is what separates an Economic World Model from an ordinary language model. At decision time t, an EWM may condition only on Ft and the candidate action at. A language model trained on a static corpus [30] can mix documents from before and after the event it is asked to predict, so its context can contain future information. The same no-peeking discipline that separates a forecasting model from a memorizing one has been the organizing principle of game-playing AI [31, 22, 21, 23], and the loss functions below make the difference explicit. For next-token modeling on a fixed snapshot, this is fine. As the primary EWM Wt without an externally imposed filtration discipline, it is not: held-out validation can only enforce filtration discipline if the holdout set is chronologically after the entire training corpus—a window that shrinks as internet-scale models train on ever more recent data. This results in very little data left for validation, and even less for robust benchmarking. Consequently, measured performance uncertainty remains high, and the small post-corpus window provides negligible information about how the model adapts to changing market regimes. The outcome is slower compounding of capital and structurally riskier decisions. A general LLM that is wrapped in a strict post-cutoff evaluation harness can still serve as a component or proposal mechanism; the categorical claim is about the bare model, not the wrapped system.

LLLM(Θ)=i∑ℓ(pΘ(xi∣ctxi),xi)(permutation-invariant over documents)

LEWM(Θ)=τ∈Ieval∑ℓ(Pτ(oτ+1,Rτ+1∣Fτ,aτ),(oτ+1,Rτ+1))(information order matters)

Suppose a language model is trained on a 2024 internet snapshot that contains articles, analyst notes, and Wikipedia edits explaining a market event from 2022. When that model learns the 2022 event, it can absorb the 2024 retrospective explanation of what happened. A filtration-respecting prediction model cannot do that: in a 2022 backtest, the training data must contain only information available up to the 2022 timeline.

Channel-Specific World Models

In principle the firm has one joint EWM Wt over the entire corporation–environment state. In practice that joint object is approximated by a collection of channel-specific world models, each trained on its own channel history Htk. These per-channel transition models are usually much simpler than a full simulator—a scaling law, a market-impact curve, a refit-decay model, or a search law is already a channel-world-model fragment. The split is a practical approximation, not a claim that the channels evolve independently; cross-channel coupling re-enters when the controller composes the rows of gt below.

Definition 11Channel-specific world model

In principle the firm has one joint EWM Wt over the whole corporation–environment state. In practice, a channel-specific world model is the channel-k conditional law over the next channel observation and reward, given the channel history Htk and a candidate channel action atk:

(ot+1k,Rt+1)∼Wtk(⋅Htk,atk),k∈{I,S,U,Z,Θ}.

Example

Suppose the corporation keeps an Investments-channel world model, WtI, trained specifically to forecast the value of assets available for purchase and how much trading them will impact their price. An Investments-specific world model asks: if the rest of the firm is held constant and the firm maintains a candidate portfolio I, how much expected equity growth will it produce?

The Portfolio Optimizer

Choosing how to spread a fixed pool of capital across competing assets so as to maximize a long-horizon utility of wealth is the canonical problem of portfolio optimization, with a literature that runs from Markowitz mean–variance allocation [32] and Kelly’s growth criterion [18], through Sharpe’s reward-to-volatility ratio [33] and Merton’s continuous-time program [34], to universal portfolios [35], robust mean–variance allocation [36], and the broader machinery of convex optimization and constrained stochastic optimal control [37, 16, 17]. The problem the corporation solves at each cycle is a multi-period instance of the same family: the channels of Ξt are the assets, at is the rebalancing trade, and Jt is the long-horizon log-utility. The novelty is the asset set: the firm allocates not only across tradable instruments but across sensors, actuators, parameters, and R&D on the same dollar axis.

We adopt the standard framing of model-predictive control: the EWM Wt supplies forecasts under candidate actions, and the policy G chooses the next allocation by solving a single-cycle convex inner problem over the per-channel return posteriors, then committing the chosen action and re-solving in the next cycle [38, 37, 16]. This section states the corporate optimization problem in its convex form and introduces the marginal-return vector that the rest of the blueprint estimates row by row.

The Corporate Optimization Problem

Stitching together the cumulative objective and the firm’s solvency, liquidity, and budget constraints gives the corporate program: the controller G picks the action that maximizes Jt subject to the constraints in the appendix. The full constraint set is collected in Program Constraints so the body can stay focused on the convex inner program.

Definition 12Corporate optimization problem

The corporate optimization problem chooses the policy G that maximizes the cumulative objective Jt, subject to budget, channel-liquidation, liquidity, and solvency constraints.

G∗=argGmaxJts.t. financial constraints.

Example

Suppose at cycle t AlphaFund has Kτdeploy=$2M and faces a candidate policy that proposes $900K investments, $400K sensors, $300K parameters, $250K R&D. The cumulative objective Jt is maximized at this allocation provided all four constraints clear: total spend $1.85M ≤ $2M (budget binds slack), no channel falls below its liquidation floor, and the liquidity and solvency reserves of Program Constraints are intact. If the proposal had instead been $2.2M, the budget constraint would bind first and the optimizer would reject the policy before any marginal-return comparison.

The Marginal Return Vector

Differentiating the common objective Jt with respect to the capital-allocation vector turns heterogeneous interventions—a researcher hire, a new alternative-data feed, a GPU, a position in AAPL, an execution-latency upgrade—into directly comparable marginal rates. Each entry of gt is the expected log-equity growth per marginal dollar invested in that channel; at the optimum every funded channel equates the same risk-adjusted shadow price of capital, gtk/σtk=λS,t∗ (Portfolio Optimization), which collapses to the bare equimarginal identity gtk=λt∗ only in the risk-neutral limit (κt→0, or per-channel dispersions σtk→0). The risk functional itself is general: Trsi Net writes the full corporate t-RSI in terms of any auditable uncertainty functional Ut, of which standard deviation is just the operational default. The next section instantiates this row by row for the quant firm.

Definition 13Marginal-return vector

The marginal-return vectorgt is the gradient of the cumulative objective Jt with respect to the cycle-t capital-allocation vector at. Each coordinate of gt tells the optimizer how much expected log-equity growth one extra dollar buys in that channel right now.

gt=∂at∂Jt

Example

Suppose the firm’s current estimates are gtS=0.2 per dollar (sensors) and gtI=0.1 per dollar (investments). Then the next $100 should go to sensors: $20 of expected future log-equity growth versus $10 from putting that $100 in the trading book.

For each channel k, we use the chain rule to expand the per-channel marginal returngtk along the trajectory through which a cycle-t dollar propagates. The equity sensitivity ∂Rτ/∂Ξτ says how much next-cycle reward changes when the corporation state moves; the propagation Jacobian ∂Ξτ/∂atk says how a dollar spent on channel k at time t moves the state at time τ. Summing their product over the planning horizon gives the dollar’s full contribution to Jt:

gtk=τ=t∑T+t−1∂Ξτ∂Rτ∂atk∂Ξτ

Example

Suppose AlphaFund onboards an IEX D-Limit route this cycle. That route enters Ut+1,Ut+2,… and shaves friction off every rebalance from then on. Each future τ contributes one term to gtU through ∂Rτ/∂Ξτ and ∂Ξτ/∂atU, so a route that pays back across thirty rebalances is priced as the sum of all thirty marginal contributions, not just the next one.

The horizon T introduces uncertainty into this pricing: the variance of cumulative reward ∑τRτ propagates through the rollout. T is therefore set at the point where additional cycles no longer meaningfully tighten the estimate once that propagating uncertainty is accounted for. This uncertainty is fundamental to the controller’s allocation problem: an honest pricing of capital must trade off the central tendency of forecasted returns against their dispersion. The most general statement of this is expected-utility portfolio optimization, which evaluates allocations under whatever utility functional the firm chooses over the joint distribution of channel returns. Under the simplest case of normally distributed returns this collapses to mean-variance portfolio optimization[32] and the per-channel Sharpe ratio gtk/σtk[33]—the form we use throughout the rest of the paper for simplicity; in production, more complex utility-of-distribution objectives are often preferred.

Portfolio Optimization details why this uncertainty necessitates the risk-adjusted form not only for the investment channel, but for the performance and optimal allocation of every channel.

Experimental Evidence of t-RSI

Thus far we have talked about a theoretical framework for probabilistic recursive self-improvement. Now we will present experimental evidence that this framework is operational. Trsi Net formally defines t-RSI as the signal-to-noise ratio of net improvement; the remaining subsections then estimate the marginal-return vector gt for the quant firm, taking each row of Ξt—investments, sensors, actuators, parameters, and R&D—in turn. Each subsection opens with the channel’s history Htk and channel-specific world model Wtk, derives the corresponding row of gt, and reports the fitted parameters that the controller of the previous section consumes. Investments is the only instantaneous row whose return is read directly off the broker statement; the other four are state-flow channels whose payouts arrive over future cycles and are therefore priced through the trajectory chain rule. The empirical content—data scaling, loss-to-edge linearization, the Chinchilla-style joint surface, the 929-experiment auto-research log law, and the continual-learning intersection—is what makes the marginal-ROI comparison of the previous section operational rather than rhetorical.

What t-RSI Measures

Why t-RSI is the thing to measure.

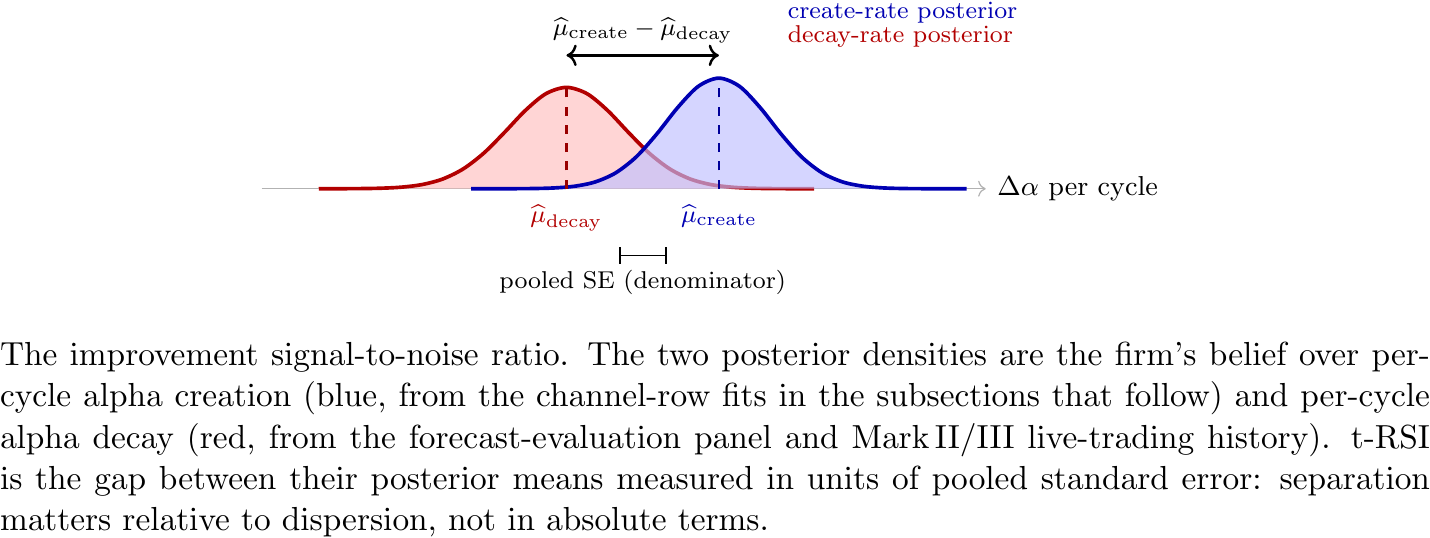

The differentiable-corporation thesis says the firm carries two posteriors at every cycle: one over alpha created per dollar spent on each channel, and one over alpha decayed from the deployed book. A controller that compounds is one that commits capital only when those two distributions are confidently separated — it believes it will create more alpha next cycle than the alpha already on the books erodes, and it believes it by enough margin that the call is unlikely to be noise. We call that standardized separation the improvement signal-to-noise ratio, written t-RSI by analogy with a two-sample t-statistic. The two distributions are not draws from one underlying process: they are posteriors over two different processes (create from the channel-row fits below, decay from the firm’s forecast-evaluation and live-trading panel). t-RSI is therefore framed as a standardized distance, not a hypothesis-test instrument.

Figure 2. The improvement signal-to-noise ratio. The two posterior densities are the firm’s belief over per-cycle alpha creation (blue, from the channel-row fits in the subsections that follow) and per-cycle alpha decay (red, from the forecast-evaluation panel and Mark II/III live-trading history). t-RSI is the gap between their posterior means measured in units of pooled standard error: separation matters relative to dispersion, not in absolute terms.

A positive t-RSI of, e.g., 2.5 means the create-rate posterior is centered 2.5 pooled standard errors above the decay-rate posterior. The firm’s controller does not commit capital to a candidate until that statistic clears a sealed-evaluator threshold (Certificate of monotone improvement); that gate is what makes compounding survive selection, and what distinguishes a self-improving corporation from one that promotes drift on noise. Equivalently, every row of the channel table below contributes one slice of the blue density, and the cycle’s investment decision is a draw from which slice the controller will pay for next.

Headline definition.

Write Δαcreatet:H for the firm’s posterior alpha creation over horizon H (the sum of per-channel contributions, with bookkeeping fixed in t-RSI Measurement Conventions), and Δαdecayt:H for the matching alpha-decay posterior. t-RSI is the standardized distance between them:

The channel-by-channel decomposition of Δαcreatet:H as a path integral along the planned allocation path, and the bootstrap propagation that supplies each SE, live in t-RSI Measurement Conventions; the operational walk-through of the headline three-month calculation lives in Three-Month t-RSI Calculation.

What the data presently say.

Empirically the firm’s own panel measures the decay rate as small and near zero. The data-derived headline reads λdecay from a per-asset alpha-decay estimator that fits the held-out forecast edge against deployment age once per asset and aggregates the resulting per-asset rate distribution robustly across the held-out asset universe (median + MAD/IQR summary; SE combines within-asset-cell dispersion with between-cell variability over training-run seeds and forecast horizons). The same qualitative picture holds in production: across 16 months of cumulative Mark II and Mark III live trading, every linear, rank, and distributional trend statistic against deployment age returns κ near zero. The data-derived headline t-RSI is therefore dominated by create-side dispersion, not by decay. The subsections that follow estimate the per-channel create-rate distribution one channel at a time; Headline t-RSI composes them into the headline t-RSI for the current operating point.

Investments as an Asset

What this channel is. Investments are the firm’s current production channel: capital positioned in the trading book and rebalanced by the controller. The EWM slice for this channel forecasts price-change distributions. Construction, scaling laws, and held-out benchmarks are deferred to a forthcoming companion paper; the empirical claims in this paper are channel-decomposed and do not depend on the companion-paper architecture. The controller turns those forecasts into a rebalance; the market function turns the rebalance into realized cash. This is the only row whose one-cycle return is observed directly from the broker ledger rather than inferred counterfactually [38, 39, 40, 41, 42, 43, 44, 45, 46].

Definition 15Investment marginal return

The investment marginal returngtI is the gradient with respect to the candidate trade ΔIt of expected return-per-dollar minus the learned execution friction ϕt. Investments are the only instantaneous channel: the gradient sees a single cycle because positions are marked to cash at the end of it.

gtI=∂ΔIt∂[atIΔItμt−ϕt(ΔIt,Ut,Et)]

Example

Suppose the EWM forecasts μt=8 bps for a $1M long in AAPL over the next bar against ϕt=3 bps of expected round-trip friction. Then gtI≈5 bps per dollar at this trade size. Doubling the size pushes ϕt up (slippage convex in size); the size optimum is where gtI falls to the marginal ROI λt∗.

What this means. The investments row tells the controller what one extra dollar of trading capital is worth right now: forecast edge μt on the candidate trade, minus the learned execution friction ϕt paid at execution. Of the three terms in Investment marginal return, the EWM forecast and the size dependence of ϕt are estimable from a backtest; the remainder of ϕt is not, and is the proprietary surface the rest of this subsection explains. Two of the three terms are public; one is not, and that asymmetry is why the live track record matters more than the backtest figure for this row.

Backtest.

ϕ deserves special emphasis: it mostly cannot be estimated from a backtest. Market impact admits a square-root-law approximation (Investments Supporting Equations), but the remainder—routing quality, venue- and broker-specific spreads, financing, adversarial response—is venue-, instrument-, size-, and time-of-day-specific and can only be learned by trading. The firm has executed approximately $400M of trades; that volume is the data behind its internal ϕ surface, which is proprietary for exactly the reason Investment marginal return makes plain—ϕ is the term the rest of the world cannot buy. The dated three-deployment-generation track record (Mark I/II/III) is reported in Deployment Parameters.

Sensors as an Asset

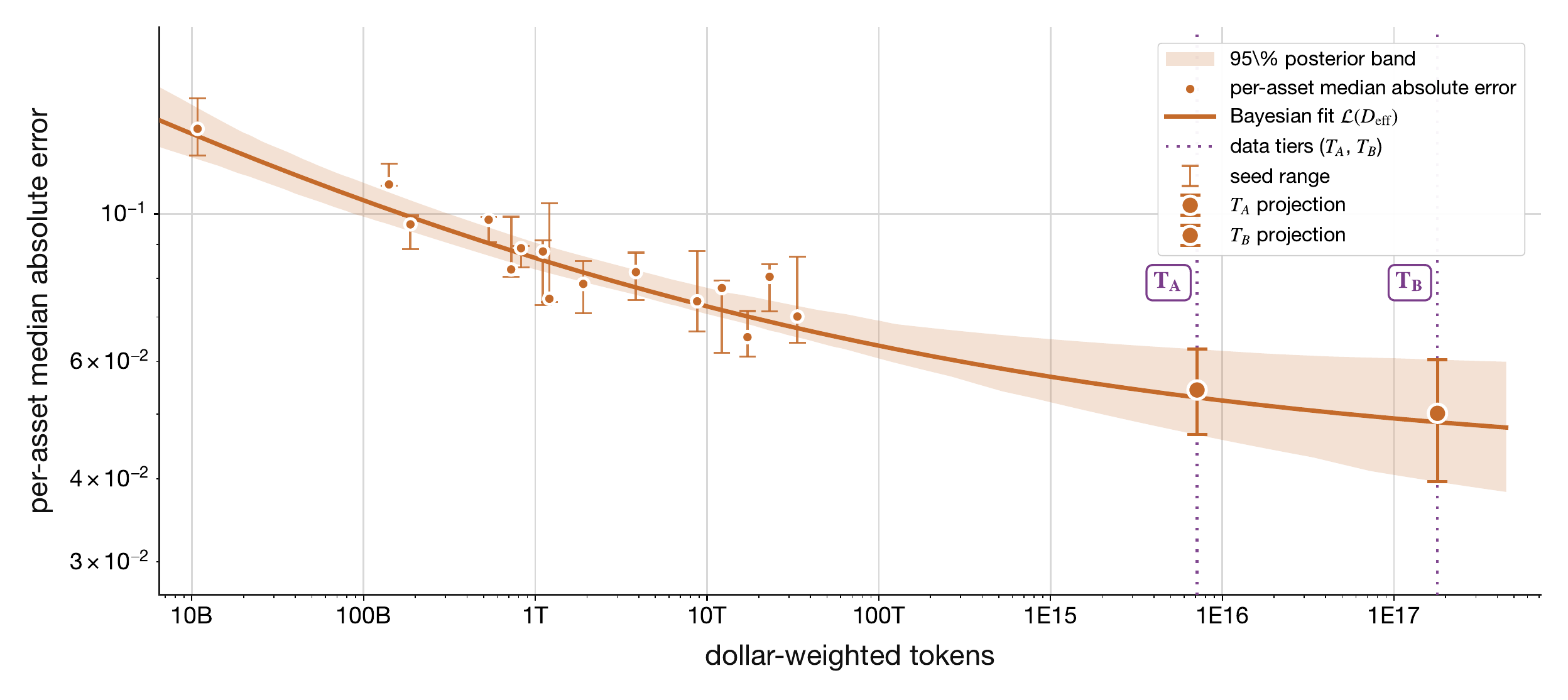

What this channel is. Sensors are purchases that enlarge the filtration Ft: market-data feeds, historical records, finer sampling, and any measurement that lets the EWM condition on more of the world. The empirical primitive is the data-scaling law, fit on the Muennighoff effective-data axis and the Hoffmann/Kaplan loss form [30, 9, 47, 48], with the underlying unit being the dollar-weighted bar in the spirit of information-driven sampling [49, 50, 51]. The body keeps only the local loss slope with respect to effective data; the fit protocol, prior choices, and controller-level chain rule are collected in Sensors Supporting Equations.

Definition 16Local data-scaling slope

The local data-scaling slope is the measured sensor primitive: how predictive loss changes when the effective dollar-weighted-token axis grows by one log-base-10 decade. The slope is the data-scaling decay rate times the reducible loss still available to be removed.

Deff∂Deff∂Lpred=−αDeff(Lpred−Lnoise)

Example

Suppose the fitted multi-seed sensor slope is αDeff=0.075 and the reducible loss component at the current Deff is ADeffDeff−αDeff=0.012. The local slope ∂Lpred/∂log10Deff=−αDeff⋅ADeffDeff−αDeff≈−9.0×10−4 per decade of Deff: each additional decade of effective dollar-weighted tokens removes about 9×10−4 of loss at this operating point, falling as the reducible component shrinks toward Lnoise.

Figure 3. Dollar-weighted tokens vs loss

Fitted parameters.

parameter

value

95% CI

R2

n

αDeff

0.156 (dimensionless)

[0.09, 0.229]

0.7619

45

R⋆

4.306 (epochs)

[2.324, 6.231]

0.7619

45

Lnoise

0.042 (loss)

[0.024, 0.061]

0.7619

45

ADeff

3.266 (loss scale)

[0.8072, 16.87]

0.7619

45

Equation

L(Deff)=0.042+3.266Deff−0.156

Deff=UD$[1+4.306(1−exp(−(E−1)/4.306))]

What this means. The fitted exponent says how much predictive error remains after the firm buys another decade of effective data. At the reported operating point, αDeff≈0.16 means a 10× increase in effective dollar-weighted tokens multiplies the reducible part of the loss by roughly 10−αDeff, or about 0.7: the model keeps about 70% of the reducible error and removes about 30%. The interval around αDeff is the uncertainty on that local data slope, not on trading alpha. R⋆ says when repeated passes over the same data stop behaving like fresh information, and Lnoise is the residual floor that more sensors cannot remove at the current model size and architecture; R&D moves architecture and therefore moves this floor (see Sensors Supporting Equations). This is why the chart is a sensor asset measurement: it prices data by the remaining predictive loss it can still reduce.

We expect this scaling law to continue, as scaling laws are some of the most well-established results across a variety of domains; as it turns out, our preliminary evidence suggests that quantitative trading demonstrates scaling laws as well. What the chart is actually pricing (effective dollar-weighted tokens, not number of predictive factors), the realistic order-of-magnitude scaling factors available against the current operating point, and the cross-domain evidence for power-law extrapolation are collected in Data Scaling.

Actuators as an Asset

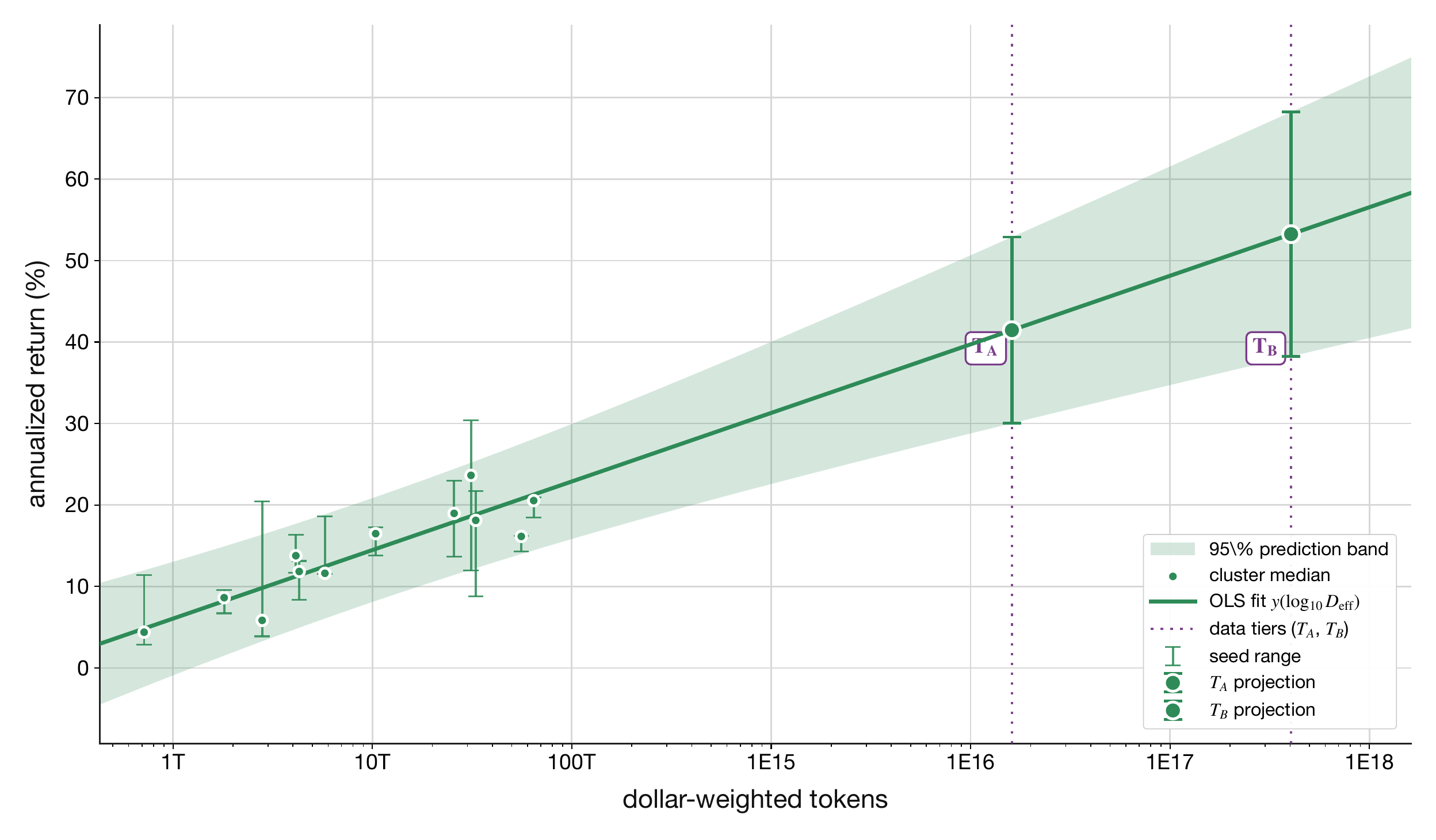

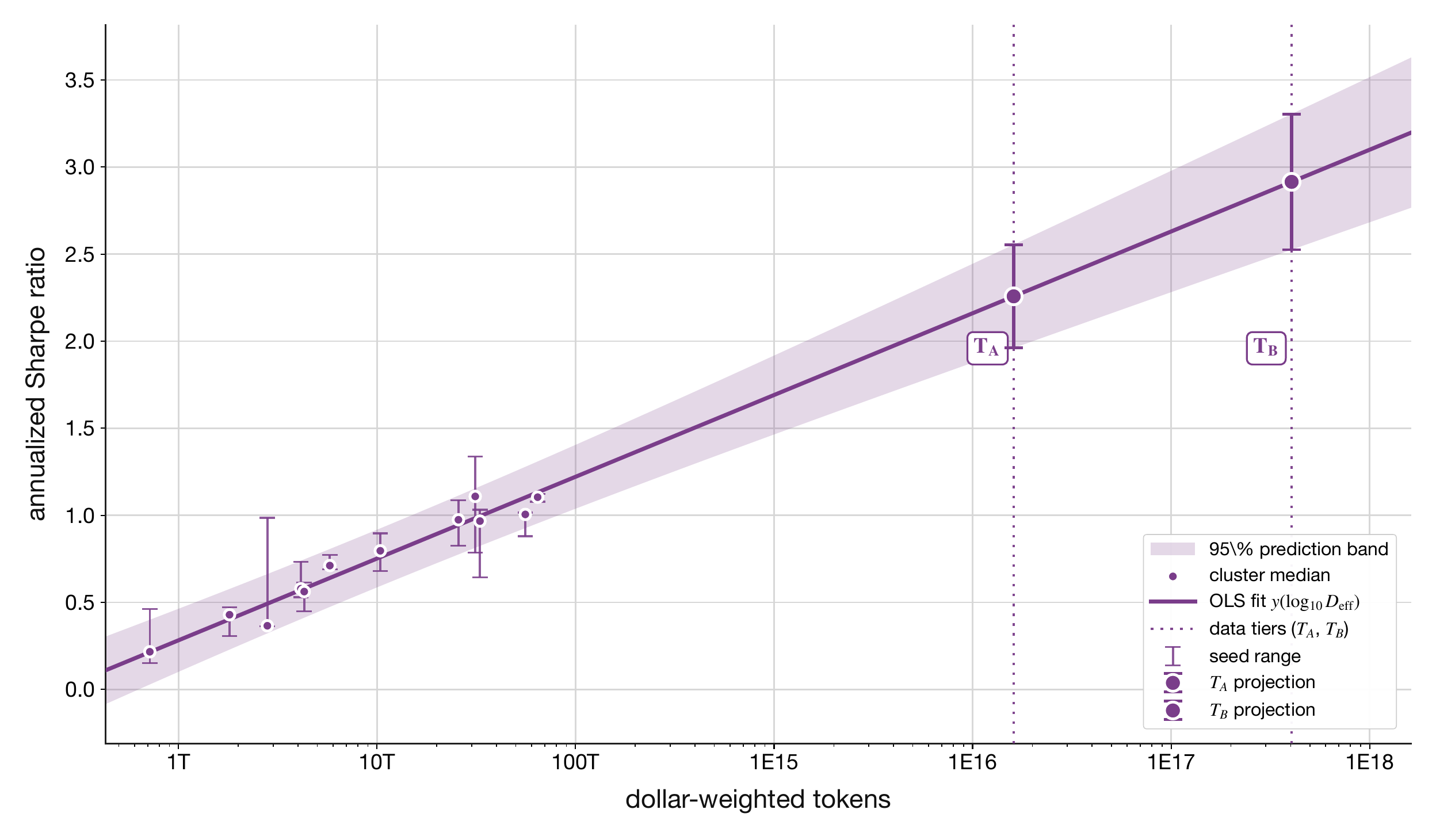

What this channel is. Actuators are the interfaces through which the controller can act. In the current quant-trading envelope, the measured actuator is the tradable asset universe: as the universe expands, the firm both trains on more dollar-weighted histories and gains more instruments through which forecasts can be deployed. The body keeps only the local data-performance slopes measured by that panel; the fit protocol, joint-path interpretation, and general actuator row gtU are collected in Actuators Supporting Equations.

Definition 17Local data-performance slopes

The local data-performance slopes are the measured actuator primitives in the current trading-envelope instance: annualized return and annualized Sharpe gained per decade of effective dollar-weighted data. In this section the actuator surface is the tradable asset universe, so the body reads these slopes directly from the panel rather than decomposing them into separate data, loss, execution, and friction terms.

Suppose the actuator panel’s OLS slope on annualized Sharpe is 0.32 per decade of Deff (cluster-median fit across the 12 universe sizes in the multi-seed scaling sweep). A universe expansion that absorbs an additional half-decade of dollar-weighted tokens predicts ∼0.16 Sharpe units of additional realized performance at the current operating point, before reserving capacity headroom against the impact baseline of Investments Supporting Equations.

Figure 4. Annualized return vs. dollar-weighted tokens.Figure 5. Annualized Sharpe ratio vs. dollar-weighted tokens.

Fitted parameters.

parameter

value

95% CI

R2

n

∂AnnRet/∂log10Deff

8.417 (pct points per decade)

[5.844, 10.99]

0.8043

12

AnnRet(TA)

41.46 (pct points)

[30.03, 52.88]

N/A

12

AnnRet(TB)

53.24 (pct points)

[38.24, 68.24]

N/A

12

∂Sharpe/∂log10Deff

0.4696 (Sharpe per decade)

[0.4027, 0.5364]

0.9499

12

Sharpe(TA)

2.258 (Sharpe)

[1.961, 2.554]

N/A

12

Sharpe(TB)

2.915 (Sharpe)

[2.526, 3.305]

N/A

12

Equation

AnnRet(Deff)=−94.96+8.417log10Deff

Sharpe(Deff)=−5.352+0.4696log10Deff

What this means. The actuator row asks whether expanding the tradable surface changes what the investment production function can do. The two slopes above are empirical between-N regressions: realized annualized return and realized annualized Sharpe per decade of effective dollar-weighted tokens. In this trading-envelope instance, the asset universe and the dollar-weighted data universe expand together, so the fitted slopes are read directly as local data-performance slopes rather than as separately identified data-only and actuator-only effects. The fitted slopes, their 95% confidence intervals, and the TA/TB extrapolation rows in the table above are all read directly off the actuator panel and the same OLS bookkeeping that draws the 95% prediction band on the chart. A note on sample size: the multi-seed sweep produces 15 universe sizes × 3 seeds =45 raw runs that anchor the sensor-row data-scaling fit, but the actuator-panel regression takes cluster medians across the three seeds at each universe size, so the n=12 reported in the parameter table is the 12-cluster-median count after dropping the three smallest universe sizes for which the per-seed median has insufficient evaluation breadth; the underlying 36-row (N,seed) panel is the object the cluster-by-N bootstrap of Three-Month t-RSI Calculation resamples. The parameter table’s n column reports the regression degrees-of-freedom unit (cluster medians), not the raw run count.

Potential scale.

We estimate the actuator-row scaling law could be extended over two tranches of source data that still satisfy the dollar-weighted-token construction of Three-Month t-RSI Calculation (dollar-denominated, strict time filtration); the corresponding TA and TB extrapolated Sharpe and annualized return are reported in the parameter table above. Tier TB is included because the underlying data class satisfies the same empirically measured dollar-weighted-token line fit that anchors Tier TA.

Tier TA – pure asset-price data: the catalogue of asset prices, quotes, trades, and order-book snapshots already commercially available across data brokers (global equities, futures, FX, rates, options, crypto, OTC fixings).

Tier TB – broader dollar-denominated time-series data: any other dollar-denominated series with a strict time index that respects the filtration (card panels, payments and settlement flows, insurance-claims tapes, payroll feeds, satellite- and geolocation-derived activity counts, public budget and procurement records), not restricted to tradable asset prices.

R&D as an Asset

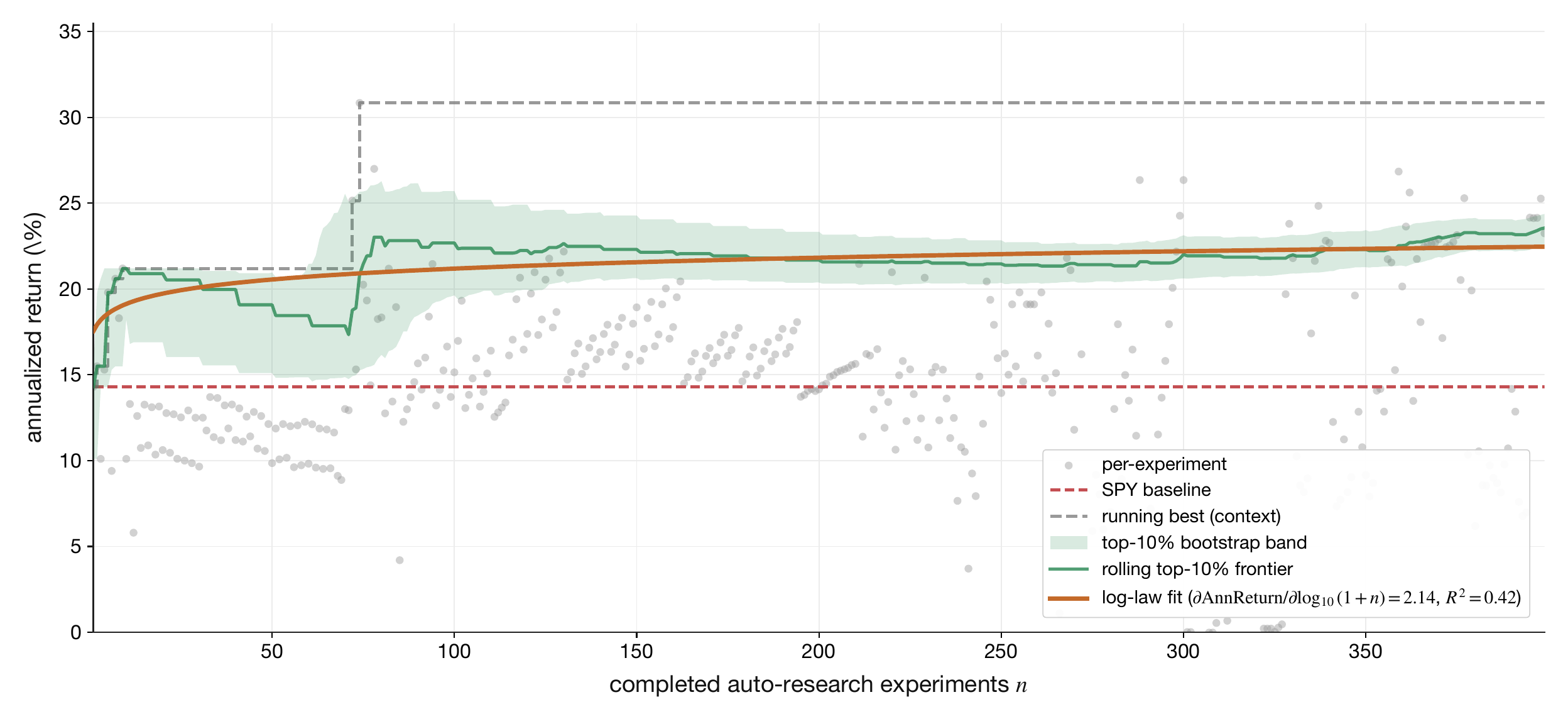

What this channel is. R&D is purchases that improve future search cycles: researcher labor, LLM API spend, GPU-hours, evaluation infrastructure, and search tooling. The empirical primitive the body reports is the derivative of the selected rolling upper-tail held-out frontier with respect to completed auto-research experiments, fit on the same axis for two metrics simultaneously — annualized Sharpe ratio and annualized return. The whitepaper manifest pins the headline frontier to the top-10% rolling upper tail for both Sharpe and annualized return, while the appendix reports the surrounding cutoff sensitivity scan. The held-out window is the canonical 1258-day validation split each campaign run reports against the 2516-day training period (see Channel Derivations); the §5.3/§5.4 sensor and actuator panels are evaluated on their own held-out splits as documented in Data Scaling. The body keeps only those two local derivatives; the dollar-to-experiment production function, the human/LLM allocation split, the architecture-quality scalar Γt, the search-scaling law Γt=ξlog10(1+Ntexp/N0), the chain rule gtZ, and the R&D transition law are collected in Channel Derivations.

Definition 18Experiments-performance slope

The experiments-performance slope is the body primitive for R&D: selected rolling upper-tail frontiers of validation Sharpe and validation annualized return across the strict-invalid- and sealed-holdout-filtered auto-research cohort, each regressed against log10(1+n) where n is the experiment index after sorting by run identifier. The headline derivatives ∂Sharpe/∂log10(1+n) and ∂AnnReturn/∂log10(1+n) report the gain on the selected frontier per decade of completed experiments; the matching intercepts β0,Sharpe and β0,AnnReturn pin the level at the start of the campaign.

Figure 6. Validation Sharpe vs. completed auto-research experiments. Per-experiment values are the gray scatter, the muted step is the running-best context line, the shaded band is the bootstrap interval for the selected top-10% rolling upper-tail frontier, and the orange curve is the selected log-law fit.Figure 7. Validation annualized return vs. completed auto-research experiments. The headline frontier is the selected top-10% rolling upper-tail fit; the running-best step remains only as muted context.

Fitted parameters.

parameter

value

95% CI

R2

n

β0,Sharpe

0.3921 (Sharpe)

[0.2258, 0.4964]

0.7563

326

∂Sharpe/∂log10(1+n)

0.3436 (Sharpe per decade of experiments)

[0.2978, 0.4153]

0.7563

326

β0,AnnReturn

16.91 (pct points)

[10.42, 19.12]

0.4159

399

∂AnnReturn/∂log10(1+n)

2.135 (pct points per decade of experiments)

[1.202, 4.792]

0.4159

399

Equation

Sharpefrontier(n)=0.3921+0.3436log10(1+n)

AnnReturnfrontier(n)=16.91+2.135log10(1+n)

What this means. The two fitted derivatives say what a ten-fold increase in completed auto-research experiments buys on the selected held-out frontier: ∂Sharpe/∂log10(1+nexp) Sharpe ratio points and ∂AnnReturn/∂log10(1+nexp) percentage points of annualized return. Each is the headline R&D primitive in the metric the firm actually optimizes against. The fitted curves are read off the report-selected top-10% rolling upper-tail frontiers of the strict-invalid- and sealed-holdout-filtered cohort; the running-best step remains in the figures only as muted context. Starting from the current campaign count ncurrentexp and projecting forward to ncurrentexp+Δn completed experiments, the additional Sharpe purchased is ∂log10(1+n)∂Sharpe[log10(1+ncurrentexp+Δn)−log10(1+ncurrentexp)], and the additional annualized return is the analogous local increment with ∂AnnReturn/∂log10(1+n). This is how the R&D row enters the t-RSI numerator: a marginal R&D dollar is priced through how many additional experiments it buys (Channel Derivations) and how much each completed experiment is currently shifting the selected frontier along the fitted curve.

Selection vs. structural scaling.

Across 929 auto-research experiments, the rolling top-10% frontier of held-out Sharpe rises log-linearly with completed-experiment count (slope ≈0.34 per decade). We note this is a selection statistic rather than a structural scaling law: the top-k% mean of n samples from a stationary distribution would also grow with n. The substantive question is whether the underlying distribution is shifting — for which the running median (rather than the top-10%) is the cleaner diagnostic, and we treat the present fit as a directional finding to be confirmed against that diagnostic in subsequent campaigns.

Why this fit, given that caveat.

The empirical methodology for studying auto-research is itself new: the only large-scale precedents we are aware of are the open-source single-GPU agent loop catalogued by [52] and the autonomous-R&D-capability evaluation harness of [53], neither of which prescribes a settled frontier-estimation protocol. Within that gap we have chosen a rolling top-quantile with a bootstrap confidence band rather than the more common running-best step. Running-best is a strict order statistic over an ever-growing sample: it is monotone in n by construction and is exactly the selection-bias regime that the deflated-Sharpe / backtest-overfitting literature documents as untrustworthy ([54, 51]). A rolling top-k% tail mean is a smoother, less brittle envelope of the same upper-tail behavior, and reporting a bootstrap CI alongside it surfaces the residual selection inflation directly. We do not claim this estimator is the right answer for auto-research scaling — only that it is a more defensible reading of the frontier than the running-best step at the same sample sizes, and that the eventual structural test against the running median (above) is what would convert it from a directional finding to a settled fit.

Parameters as an Asset

What this channel is. Parameters are model scale purchased through training compute. The marginal-return row sits on the joint Hoffmann/Chinchilla loss surface [30, 9]: an architecture-set noise floor, a model-size term, and a data term whose coefficients are pinned by a (Mt,Dt,At) sweep. The body keeps only the joint surface; the full chain-rule decomposition gtΘ, the compute-cost identity, and the worked example are collected in Channel Derivations. The complementary empirical question — how quickly deployed parameters go stale, i.e. the alpha-decay term that prices the cost of not refreshing Θt — is what the deployed history already lets us measure, and we report that here.

Definition 19Parameter marginal return

The parameter marginal returngtΘ chains parameter dollars → model size Mt→ predictive loss → expected return → objective. The model-size term is the Hoffmann/Chinchilla power law Parameters Joint Scaling; the divisor DtseenKtpass/ηttrain is the compute-cost identity Compute Cost Identity that converts an Mt slope into a dollars slope.

Suppose AlphaFund is currently training a 2×107-parameter EWM and is considering a 4× scale-up at fixed Dt. Under a Chinchilla αM(At)≈0.34, the model-size contribution to Lpred shrinks by roughly 1−4−0.34≈38%. Whether that is bought depends on the matching Dt side of the joint surface; the model-size sweep that pins αM(At) has not yet been run, so the parameter row is recorded symbolically.

What this means. With the model-scaling slopes still pending, the deployed evidence speaks to the other half of the parameters row: not how steep the loss surface is in Mt today, but how fast the deployed weights Θt themselves age out. That is the αdecay term the controller charges against every cycle the firm chooses not to refresh its parameters.

Empirical alpha-decay from parameter staleness.

The parameter row is also where the corporation books the time-rate alpha-decay term that enters Investment marginal return and the t-RSI numerator of Three-Month t-RSI Calculation. Running the forecast-evaluation panel pooled across three training-run seeds — effectively approximately three independent five-month training-run studies (127–128 assets per run, three forecast horizons, ∼150,000 held-out rows per horizon over the [2020-01-01, 2025-01-01) test window) — gives a per-asset median decay rate λeff∼2–4×10−4 per 60-minute cycle, with the per-asset Mann–Kendall slope on MAE-skill against deployment age centered near zero across the 127-asset universe. The same qualitative picture holds in production: across ∼16 months of cumulative Mark II and Mark III live trading (Deployment Parameters), every linear, rank, and distributional trend statistic against deployment age returns a κ near zero, with several leaning in the positive-trend direction. Empirically, then, the measured alpha decay sits at or below the panel’s resolution; the small magnitude is most plausibly attributable to the firm’s low ∼27× annual portfolio turnover, which holds deployed weights inside the regime where parameter drift is dominated by sampling noise. The data-derived λdecay that enters the headline t-RSI is therefore small and near zero. The per-horizon decay panels, fresh-vs-stale density panels, and per-asset λeff histogram are in Channel Derivations.

Model-scaling sweep is forthcoming.

The (Mt,Dt) Chinchilla-style grid that pins αM(At), AM(At), the training-efficiency term, and the model-size-dominates-data crossover is the obvious next sweep on the multi-seed scaling backbone. The current data lets the optimizer price decay (small, noise-dominated) but not yet model-size headroom; that sweep is queued as the next campaign and will refresh this row’s coefficients on completion.

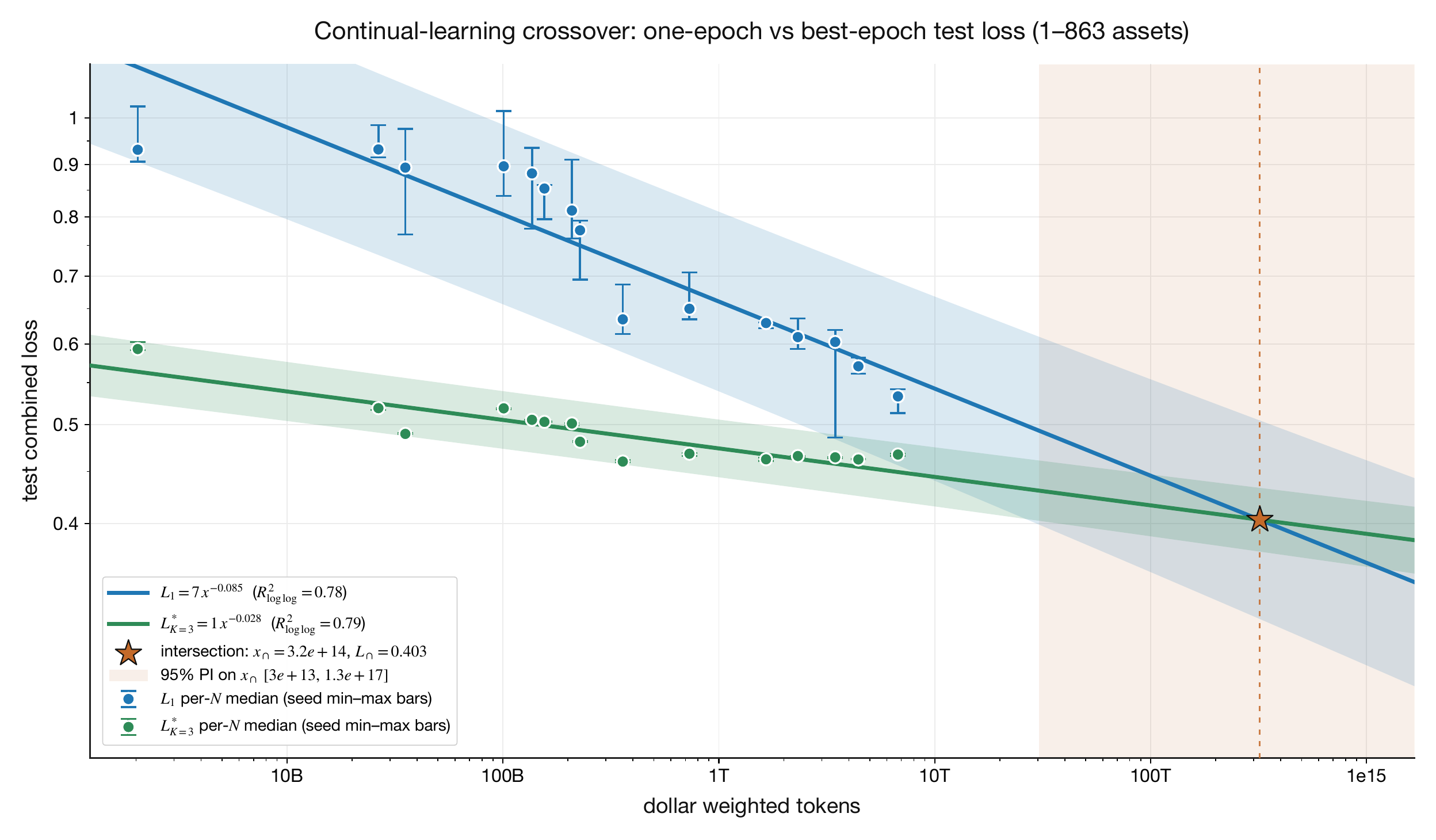

Continual Learning

The regime in which the model learns the relevant distribution in one pass, so the best validation loss after repeated epochs is no better than the loss after the first epoch. In this paper the boundary is the intersection between the one-epoch loss curve and the best-epoch loss curve. At that point epochbestloss→1: one repetition over the data is enough for the model to converge.

This is a structural statement about the parameters channel. Once the data can be learned in a single viewing, the firm exits the static train/validation/holdout regime and enters a walk-forward regime in which the deployed weights are refit every t+τ for some τ≪T, where T is the total length of the dataset. This is the same generalization regime observed at scale in modern language-model training, and operationally it is what is commonly called continual learning—data evaluated and trained prequentially, in chronological sequence.

Two consequences propagate forward. First, the variance of the expected-return estimator collapses: every training sample becomes a valid out-of-sample evaluation point at the next refit boundary, so the firm’s posterior on its own forward returns tightens monotonically with operating history. Second, the tighter posterior feeds back into both the architecture-search channel and the controller. Architecture search inside R&D gains confidence that a candidate represents a genuine improvement rather than a sampling fluke, and the risk-aware controller allocates more optimally across all five investment channels because σc,t is smaller, increasing the rate of improvement. Continual learning is therefore not just a downstream consequence of epochbestloss→1—it is also the mechanism by which the firm’s per-row uncertainties tighten.

Definition 20Continual-learning intersection

The continual-learning intersection is the dollar-weighted-token scale x∩ at which the single-pass (K=1) loss curve meets the best-of-K⋆-epoch loss curve, with both curves fit as Hoffmann-style power laws on D at fixed Mtint and shared loss floor L∞. Below x∩ the best-epoch curve is strictly tighter (additional passes over a small token budget reduce loss); at x∩ the two curves cross, and to the right of it epochbest loss →1: a single pass over the data is enough for the model to converge, so repeated epochs no longer help and most of the available history can be reserved for genuine evaluation rather than training. The two power-law exponents α1 and αK⋆ are independent and separately estimable; setting LK=1(x∩)=LK=K⋆(x∩) and solving for D gives x∩=(AK⋆/A1)1/(α1−αK⋆).

Suppose the corrected multi-seed fit puts the intersection at x∩≈3.2×1014 DWT and L∩≈0.40 test combined loss, with α1≈0.085 and αK=3⋆≈0.028. Once AlphaFund crosses this scale, the scaling-sweep architecture is in its prequential regime: train on the most recent slice, test on the rest—a holdout pattern unavailable to the multi-epoch regime.

Figure 8. One-epoch test loss and best-epoch test loss versus single-pass dollar-weighted tokens. The intersection marks the estimated entry into the Kt→1 continual-learning regime.

Fitted parameters.

parameter

value

95% CI

R2

n

α1

0.08548 (first-epoch loss slope)

[0.07194, 0.09903]

0.7805

45

αK=3∗

0.02795 (best-epoch loss slope)

[0.0236, 0.0323]

0.7867

45

x∩

3.204e+14 (dollar-weighted tokens)

[3.110e+13, 1.718e+17]

N/A

45

L∩

0.4035 (test combined loss)

[0.3028, 0.448]

N/A

45

The chart says that first-epoch loss is falling faster than best-epoch loss as the dollar-weighted-token budget grows. If those two power laws intersect, then the model no longer needs repeated passes to reach its best loss: the first pass is enough. Operationally, that means a smaller fraction of the available history is needed for training and a larger fraction can remain genuinely held out for testing. Taken to the limit, if the distribution can be inferred from a small enough slice of the data, continual learning becomes a prequential approximation: the firm learns from the latest examples while preserving most of the data stream as evaluation.

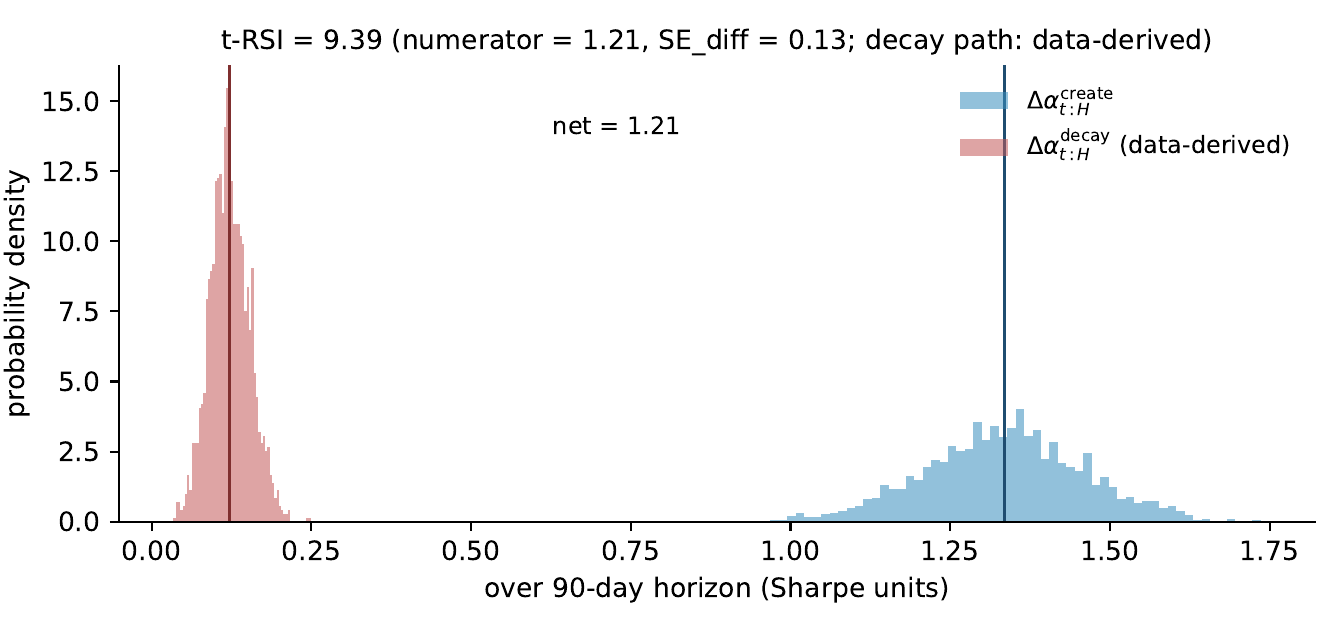

Headline t-RSI

At the current operating point the firm measures a positive standardized distance between its alpha-creation rate and its alpha-decay rate over the next quarter. Read the headline as: how many standard errors of the posterior of the difference the projected net alpha increment Δαt:Hnet sits above zero. The numerator is the difference of the posterior mean create rate and the posterior mean decay rate; the denominator is the standard error of that difference, propagated from an end-to-end bootstrap on the channel-row fits and the empirical alpha-decay panel cluster bootstrap. The headline conditions on the data-derived alpha-decay rate, which the firm’s forecast-evaluation panel and the 16 months of cumulative Mark II/III live trading measure as small and near zero (every linear, rank, and distributional trend statistic against deployment age returns a κ near zero, with several leaning in the positive-trend direction). The scope of the underlying extrapolation is narrow: the calculation only asks the data-scaling slope to continue roughly one and a half orders of magnitude past the in-sample Deff (one decade absorbed every two months over the three-month horizon), which is well inside the 3.5-OOM in-sample range of the sweep, and integrates that extension over a single three-month horizon.

Reading the magnitude.

The headline is large because the firm currently operates below the market-impact floor: at ∼$400k AUM and ∼27× annual turnover, individual orders sit well inside the regime where they can be split without measurable price impact, and the empirical impact contribution to the create-side bootstrap is indistinguishable from zero. The data-derived alpha-decay rate is also small (Three-Month t-RSI Calculation). With neither impact nor decay materially eroding the create-side gains, the standardized distance collapses to a near-pure read of the create-side dispersion, and that read is tight. A different operating point will read differently: at K-times current AUM the literature Q/ADV impact law [39, 55] reintroduces a capacity-driven Sharpe drag on the create side, and the headline compresses. Under a turnover trajectory consistent with the empirical decreasing-returns-to-scale pattern documented for active managers [56, 57], the same posterior reads 4.59 at K=10× AUM and 2.90 at K=100× AUM; under a worst-case trajectory in which annual turnover is held fixed at its current level, the headline crosses zero between K=10× and K=20× AUM. The full two-row capacity-sensitivity table is in Three-Month t-RSI Calculation. The thresholded form of this test statistic — the certificate of monotone improvement that gates whether a candidate update is admitted into the deployed model — is detailed in Improvement Certificate.

Figure 9. Posterior of the two t-RSI components over the 90-day horizon at the current operating point, under an end-to-end bootstrap of the channel-row fits. Light blue: Δαt:Hcreate, the posterior of the firm’s alpha-creation rate over the horizon (sensors+actuators plus the gross-of-carry R&D arm; researcher compensation flows through the accounting projection, not the creation-rate functional). Light red: Δαt:Hdecay, the posterior of the data-derived alpha-decay rate from Three-Month t-RSI Calculation (empirically small and near zero). The vertical solid lines mark the two posterior means; the dashed annotation is their difference. The title carries the standardized-distance t-RSI Trsi Net, the numerator (difference of means), and the denominator (SE of the difference).

Toward the Differentiable Corporation

AlphaFund is an early implementation of a differentiable corporation: a company whose operational decisions are being converted into auditable marginal-return estimates against future equity growth. In this architecture, each major use of capital—trading capital, data, execution infrastructure, model parameters, and R&D—becomes a row in a common optimization problem. The controller’s task is to compare those rows on the same dollar-denominated axis, allocate capital to the highest risk-adjusted marginal return, and update the estimates as realized outcomes arrive.

The evidence in § 5 measures several of these rows at the current operating point. Sensors and actuators are represented through data-performance scaling laws; R&D is represented through experiment-performance frontiers; parameters are represented through refit and decay measurements; and the combined create-versus-decay distance is summarized by t-RSI. These measurements make AlphaFund a concrete test case for the differentiable-corporation program.

Three Structural Facts

Pre-existing market with mandated price discovery. For t-RSI to be operationally measurable, the firm’s actions must be priced by an external mechanism at sub-cycle latency, with the prices observable and timestamped. Public equities satisfy this by federal mandate: every executed trade is reported and made public, timestamped to the nanosecond, against a market that has been continuously operating for longer than any other. The relevant point is not that this market is attractive — it is that the price-discovery machinery for every action the firm takes already exists, externally, at no construction cost and with no PMF term confounding ∂Equity/∂Company. Most candidate domains fail this condition: in nascent markets the firm has to build the price-discovery surface itself, which adds a learned-mechanism term to every gradient; in regulated-but-illiquid markets the prices exist but resolve too slowly to score per-cycle decisions. Quantitative trading is unusual in that this condition holds trivially.

Principal value capture. t-RSI requires that ∂Equity/∂Company be dominated by the firm’s own actions rather than by intermediated customer behavior. A trading firm is principal to its own predictions: carry is on the firm’s own positions against the market, not a per-call fee on a customer’s downstream use of a tool. The contrast with platform-AI clarifies what the condition rules out, not which business is preferable. A platform seller’s ∂Equity/∂Company is dominated by enterprise sales cycles, competitive substitution, and product–market fit — exogenous, lagged, customer-dependent terms whose variance swamps the marginal effect of any single internal improvement. The same model improvement that earns a platform $0.001M in API revenue might earn the principal $100M in carry; the difference is not which firm is better-run, but which firm has a directly measurable derivative against its own actions. Most industries fail this condition because their value capture flows through a customer-decision bottleneck whose noise drowns out the create-vs-decay signal the framework needs to identify, and the standard error on the relevant gradient grows accordingly.

API-complete operational degrees of freedom. Every operational decision in the firm is, in principle, a function call. Data ingestion is an API. Model training is an API. Capital allocation is an API. Trade execution is an API. Asset acquisition—new data licenses, brokerage accounts, exchange memberships—is an API. Each call produces a structured log that doubles as the causal record needed for a derivative against it. A clothing manufacturer’s production function bottlenecks on physical objects (textile sourcing, factory throughput, retail distribution); ∂Equity/∂(material blend) is not even well-defined as a derivative because the action space is not differentiable. Quantitative finance is the industry where it is.

The 15-bucket cross-industry ranking below makes this exclusive overlap explicit: quantitative finance is the only domain bucket in the top quintile jointly on theoretical LM exposure (0.94), automation-versus-augmentation occupational share (0.76), and self-reported API completeness, with high confidence [58, 59]. The AEI V4 dataset (Anthropic Economic Index) covers only 10.8% of O*net tasks by count; the missing 89% are overwhelmingly physical or manual. The empirical frontier of LM-mediated work is therefore the frontier of API-describable work—quantitative finance lies inside that hull while manufacturing, logistics, and on-site services lie outside.

Cross-industry exposure ranking across the 15 BEA-Detail domain buckets. Theoretical LM exposure is the labor-dollar-weighted AIOE LM score (Felten/Raj/Seamans). Automation share is the labor-dollar-weighted automation-vs-augmentation ratio from the AEI V4 (Tamkin et al., Anthropic Economic Index) classification. API completeness is a qualitative proxy from the upstream pipeline. Quantitative / Investment Finance (highlighted) is the only bucket in the top quintile on all three axes with high confidence.

Domain bucket

Theoretical

Automation

API

LM exposure

share

completeness

Legal Services

1.00

0.27

medium

Quantitative / Investment Finance

0.94

0.76

high

Banking & Credit

0.92

0.70

medium

Insurance

0.91

0.68

medium

Accounting & Finance Consulting

0.91

0.67

medium

Software / SaaS / IT Services

0.87

0.68

high

Data & Cloud Infrastructure

0.86

0.69

high

Management Consulting

0.81

0.70

medium

Architecture, Engineering & R&D

0.76

0.65

medium

Content, Media & Advertising

0.69

0.71

medium

Healthcare Admin-Heavy

0.62

0.63

medium

Physical Services & Trades

0.41

0.67

low

Manufacturing & Industrial

0.40

0.67

low

Logistics, Warehousing & Wholesale

0.39

0.69

low

Agriculture, Mining & Extraction

0.34

0.69

low

Channels Reinforce Each Other

The certificate of monotone improvement (Certificate of monotone improvement) fires on one channel at a time, but channels are linked through shared state, so marginal dollars do not decompose channel by channel. Formally, positive cross-partials of the cumulative objective on the active rows (Cross-channel supermodularity) yield supermodularity in the sense of Milgrom and Roberts [60]: a marginal dollar on channel j raises the marginal value of a dollar on channel k, and conversely. Local positivity can fail under capacity, attention, or saturation, so no global supermodular ordering is asserted. The continuation claim is probabilistic, not global (Certified-commit continuation bound): the certificate gates each commit at the prevailing operating point rather than relying on supermodularity everywhere, and while the cross-partials in Cross-channel supermodularity remain positive on those rows, an observed increase in the certified-commit improvement rate raises the posterior probability that the next commit also improves the loop, with the inequality read as an empirical row-law claim rather than a theorem.

Definition 21Cross-channel supermodularity

Cross-channel supermodularity says that the cumulative objective Jt has non-negative cross-partials on the rows the firm has identified [60]: a marginal dollar on channel j raises (or leaves unchanged) the marginal value of a dollar on channel k. This is a local statement on the active rows, not a global theorem; capacity, attention, and saturation can flip the sign off the operating point, which is why the continuation claim of Certified-commit continuation bound is probabilistic rather than supermodular-everywhere.

∂atj∂atk∂2Jt=0

Example

Suppose AlphaFund’s tradable universe widens from 127 to 160 names (an actuator add) while sensors absorb another decade of dollar-weighted tokens. The actuator add lifts the marginal value of the sensor dollar—more assets means more rows the new data can sharpen forecasts on—and the sensor add lifts the marginal value of the actuator dollar by raising the per-asset μt the widened surface deploys against. The cross-partial ∂2Jt/(∂atS∂atU) is non-negative at the current operating point.

Definition 22Certified-commit continuation bound

The certified-commit continuation bound is the probabilistic, row-law version of supermodularity: conditioning on a successful certified commit at cycle t—i.e. on the event Certt=1 from Certificate of monotone improvement—raises the posterior probability that the next certified commit also improves t-RSI. Read as an empirical row-law claim, not a global theorem: it says the firm’s track record of clearing the certificate is itself evidence that the next commit clears.

−Pr(Δt-RSIt+1>0,Ft)+Pr(Δt-RSIt+1>0,Ft,(31))=0

Example

Suppose the firm has cleared the certificate on ten consecutive Mark III refits, each raising the held-out three-month t-RSI by a posterior-mean 0.1 standardized units. The eleventh candidate update arrives. Conditioning on the prior ten certified commits raises the posterior probability that Δt-RSIt+1>0 above its unconditional rate; the strength of the lift is a posterior on the firm’s own row-law trajectory rather than a structural guarantee.

Drift Detection and Recovery

A differentiable corporation that keeps allocating through regime change needs three things; only the first is what section 5 measures in isolation.

That first requirement is fitted marginal-return laws with measurable standard errors on every operational degree of freedom.

The second is drift detection on the world model itself—an operational trigger when live inputs move outside the support on which those standard errors were identified.

The third is R&D throughput high enough that, once that trigger fires, the firm refits to the new regime before an obsolete mapping bleeds out deployable capital.

The certificate of Certificate of monotone improvement is evaluated on the same audited moments, so its economic content weakens exactly when drift invalidates the inferential basis for those errors.

On (2), the alpha-decay panel of § 5.8 already constitutes this surveillance and measures the decay rate as small and near zero on its measured horizon. On (3), the continual-learning construction of § 5.7 implies a refitting time constant that is short relative to the decay time constant summarized in (2), at the firm’s prevailing data-ingestion rate. The firm’s recovery rate therefore dominates its measured decay rate, which is what self-improvement under regime non-stationarity actually requires.

Definition 23Deployable-capital decomposition

The deployable-capital decomposition splits next-period equity into the slice generated internally by the realized cycle reward on the existing book (Kt+1int) and the slice supplied externally by outside investors against the firm’s certificate-cleared track record (Kt+1ext). External capital amplifies the loop only while each marginal externally supplied dollar clears the same risk-adjusted certificate of Certificate of monotone improvement after financing costs, dilution, market impact, and capacity effects.

Kt+1=Kt+1ext+Kt+1int

Example

Suppose at cycle t shareholders’ equity is Kt=$25M and the realized log-return on the existing book over the cycle is Rt=0.04, so Kt+1int=KteRt≈$26.02M. A certificate-cleared $5M outside-equity round closes that cycle (Kt+1ext=$5M), giving Kt+1≈$31.02M. If the marginal $5M had failed the certificate (financing cost above shadow price, or market-impact erosion past the capacity floor) the firm would have declined the round; the loop would have continued amplifying only off Kt+1int.

The Bitter Lesson for Capital

Sutton’s bitter lesson observes that the methods which win at scale in machine learning are the ones whose performance grows with computation, not the ones that encode hand-crafted human structure [61]. The capital analog is structurally identical and historically older: the firms that win at scale are the ones whose throughput grows with absorbed capital, not the ones whose decisions are bounded by the size of a fixed staff. The supermodular cross-partials of § 6.2 compound the internal loop at the rate the channels permit; the bitter lesson is that the loop does not stop there.

Once the corporation demonstrates, in its own operating record, that incremental capital reliably converts into measured row improvement and deployable edge, outside investors can treat that relationship itself as an investable object. The next-period deployable-capital identity (Deployable-capital decomposition) separates internally generated deployable capital Kt+1int from externally supplied capital Kt+1ext. External capital amplifies the loop only while each marginal externally supplied dollar clears the same risk-adjusted certificate after financing costs, dilution, market impact, and capacity effects.

Two things are worth mentioning. First, different financing instruments have norms—and in some cases strict bylaws—governing what they can and cannot invest in. As the world gets increasingly digitized, the instruments with more leeway and more quantitative discipline will, on average, outcompete those that cannot process as much information; this is its own selection pressure on the type of external capital a recursively improving corporation can absorb. Second, a self-improving corporation with improving capability attracts more capital; when the marginal certificate continues to clear, that increased capital further increases the rate of self-improvement, which increases the rate of returns, which in turn increases the rate of external investment. Some of that capital—particularly AUM and equity—does carry per-dollar performance decay through market impact and capacity. What matters is the race: when incoming capital buys data or architectures that raise expected return faster than market impact erodes alpha, the rate of self-improvement continues to climb and the rate of external investment accelerates with it—a positive feedback loop.

Completion Roadmap

The next phase is to close the remaining operational gradients. Salary and headcount cost, banking and cost of capital, hardware procurement and depreciation, asset-acquisition cost, and AUM acquisition cost are the remaining major terms in the corporate equation. Each term has a natural measurement surface: dollars in, operational capability out, and realized contribution to future equity growth. As those surfaces are instrumented, the corporation becomes progressively more legible to its own controller.

The completed object is a firm whose capital-allocation process is scored end to end: every major expenditure has a forecast, every forecast has a realized outcome, and every realized outcome updates the next allocation. The differentiable corporation is the limit of that process.

Beyond Quant Trading

The Economic World Model is a network trained on the joint distribution of priced economic data—a foundation model for allocation in the same sense that a large language model is a foundation model for text. Text describes economic activity; prices settle it; the same underlying forecast can therefore be executed at more than one depth in the real economy rather than only as a paper position.